Coinbase, JPMorgan Partnership Delays Drag On

Last summer, JPMorgan Chase and Coinbase announced a major partnership to tie crypto into the bank’s banking and credit card offerings. The move marked a key endorsement of the top U.S. crypto firm from the biggest bank in the country.

Nearly a year later, none of those features has gone live and the companies haven’t publicly explained the delay. Meanwhile, though the companies have maintained their various partnerships, the backdrop for launching consumer crypto products has changed dramatically—investor interest has waned as crypto markets have soured. The two firms are also clashing in Washington over crypto legislation that banks say could threaten their retail deposits, a fight that has dragged on and diminished the chance of the bill passing this year.

The companies had long found ways to do other business together despite their differences over crypto. JPMorgan CEO Jamie Dimon, who’s known for his blunt public commentary, called bitcoin a “fraud” as early as 2017 and later likened crypto to a Ponzi scheme. But his skepticism didn’t stop JPMorgan’s bankers from moving early to win business from Coinbase. Coinbase was one of JPMorgan’s first crypto-industry commercial banking and treasury clients at a time when many other banks saw the sector as too risky. That paved the way for JPMorgan’s work on Coinbase’s 2021 direct listing.

More recently, as the Trump administration pushed to move crypto into mainstream finance, JPMorgan embraced crypto more directly with planned offerings for its small and big customers alike.

In July 2025, JPMorgan and Coinbase announced plans to “make buying crypto easier than ever,” in part by allowing Chase banking customers to fund their Coinbase accounts by tapping their Chase credit cards. That feature was supposed to go live by fall 2025. And by this year, the companies said, customers would be able to link their Chase bank accounts directly to their Coinbase wallet and convert points earned through Ultimate Rewards, the bank’s popular card rewards program, into funds for buying crypto.

For Coinbase, the deal promised easier access to JPMorgan’s more than 80 million consumer customers. JPMorgan at the time was also seeking to charge fees to data aggregators that access Chase bank account information in order to provide a connection to outside apps. A direct integration with Coinbase would have offered the bank a way to connect its customers’ accounts to the crypto giant without third-party data aggregators.

Crypto markets were also hot back then, boosting the appeal of a consumer tie-in, and the regulatory environment was making banks more open to digital assets broadly. The price of bitcoin had just hit a new record high, close to $120,000. Stablecoins, essentially digital dollars, were being hailed as the future of finance. And the House had just passed the Clarity Act, meant to provide clear rules for the crypto, with broad support from the crypto industry.

The two companies also were deepening their ties for services aimed at large customers. Last November, JPMorgan publicly launched a U.S. dollar-denominated deposit token, JPM Coin, issued on Coinbase’s public blockchain. The bank touted the launch as a way for big clients to move money instantly, 24/7.

JPMorgan also lined up Coinbase to provide custody services for a planned JPMorgan lending product that would let the bank’s large clients borrow money using their crypto holdings as collateral, people familiar with the partnership said. That lending program was reportedly supposed to launch by late 2025. It hasn’t gone live yet.

But tensions between the crypto and banking industries were building. As the Senate was drafting its own version of the Clarity Act in late 2025, banks large and small pressed lawmakers to restrict the rewards that crypto firms pay consumers for holding stablecoins.

Banks argue that the effectively higher interest rates stablecoins offered could prompt consumers to move cash out of bank accounts. That would undercut a key source of cheap bank funding, and banks say the more lightly regulated crypto firms have an unfair advantage. Crypto firms, on the other hand, argue that banks are trying to stamp out competition.

A January Senate draft of the bill sided more with banks on that point, prompting Coinbase CEO Brian Armstrong to withdraw the company’s support. The following week in Davos, Dimon interrupted a meeting between Armstrong and former U.K. Prime Minister Tony Blair, reportedly telling the Coinbase chief, “You are full of shit.”

The Senate banking committee advanced the bill in May, but it has yet to receive a full Senate vote. Sparring between Dimon and Armstrong has continued. “No one is going to bow down to this guy, OK, or that company,” Dimon said in a Fox Business interview in May, referring to Armstrong. In June, Armstrong told Politico it “was kind of sad” to hear Dimon’s slap down.

Meanwhile, a crypto sell-off in recent months has spooked small investors away from the market. Coinbase laid off 14% of its staff in May, and its shares have tumbled 50% over the past year. Bitcoin recently dipped below $60,000, less than half its level last fall.

Right now, there’s no option for a user to add a Chase credit card to Coinbase’s payment methods. Chase customers remain unable to link their Coinbase account to their bank account, though they can link to other apps like Robinhood. And if you ask Coinbase’s virtual assistant whether you can transfer Chase points, the AI assistant says: “No—Coinbase can’t accept transfers of Chase Ultimate Rewards points directly into a Coinbase account (Coinbase only supports deposits in supported fiat currency and crypto, not credit card/rewards points).”

The companies did not elaborate on the consumer banking delay or provide an updated timeline for any launches. A Chase spokesperson said the company doesn’t “share specifics on ongoing business conversations with our partners.” A JPMorgan spokesperson declined to comment on the status of the crypto lending program.

A Coinbase spokesperson said: “Our banking, treasury, commercial and all other relationships and partnerships with JPM are very strong. The partnership product integrations are not on hold but are delayed. We look forward to rolling these features out soon.”

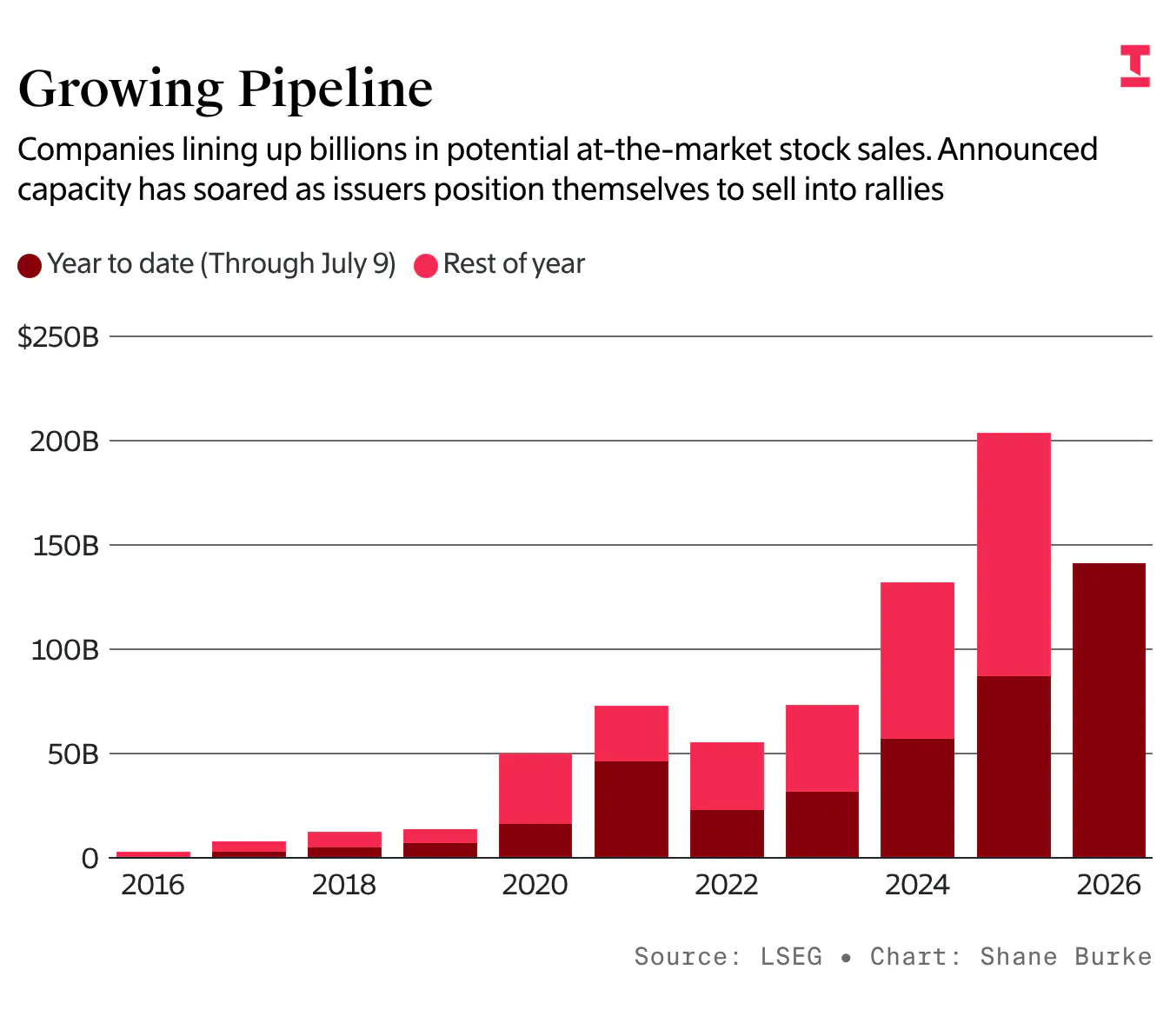

The Big Number: $141 Billion

That’s the value of potential at-the-market stock sales announced by U.S. companies as of July 9, according to LSEG data, up 62% from the same point last year. The data tracks authorized ATM program capacity, as opposed to actual shares sold, across U.S. issuers including conventional public companies as well as REITs, business development companies and closed-end funds.

ATMs, where public companies sell shares into the open market, have been popular in recent years with meme stocks and crypto treasury firms. More recently, AI-related companies like IREN and Supermicro are also lining up to sell shares this way. That announced capacity doesn’t mean all the shares will actually be sold, however. As we covered this weekend, companies are betting on strong investor support and sustained stock price rallies to fund their ambitions gradually.

The drawback, compared with traditional underwritten follow-on equity offerings, is that ATMs don’t lock in the funding up-front, leaving companies exposed to a market reversal before they can complete the sales. It’s a pipeline worth keeping an eye on!

New From Our Reporters

The Hot Equity Trade Spreading Through the AI Boom